R.W.E. of the J.B.O. wrote:OHV notec wrote:However, I'm not opposed to paying a little more if it means people won't be denied for pre-existing conditions, and if students can remain covered under their parents' plans through college, etc. I truly believe this was a step in the right direction.

Cases, such as people only buying after getting sick, obviously need to be dealt with still. I can only hope that these issues are addressed by future legislation, just as I can only hope all the frivolous lawsuits will be addressed. It's not like things can't be revised in the future. Just like AZ SB1070 was severely lacking initially, things can be fixed.

It's not going to be a little more, it's going to be a lot more, for the reason I stated. It's going to be abused.

As for future legislation fixing it, this is something I'm against.

I think this is idealistic beyond reason. A revision of health care this far-reaching simply cannot be completely figured out before it even hits the streets. The only way to fully understand the impact and effects of such a quantum shift is to implement some reasonably executable version, and then fine-tune it as practical experience can only then dictate. The quest for a "perfect" solution, at a time when it's humanly impossible to know what perfect would be, is one of the reasons the bill was tied up for so much longer than it needed to be.

R.W.E. of the J.B.O. wrote: I would like to point out that you just blew a hole in the theory of the increase in revenue being due to the population growth, though.

Let's be clear on this: population increase is ONE reason for the revenue increase...not

THE reason. Gaining approximately 30 million new citizens in ten years (a 10% increase in merely 4% of the nation's years of existence) definitely hits the bottom line.

R.W.E. of the J.B.O. wrote:OHV notec suggested it was because of the housing bubble, but that was already in play years before as well. I am curious if he had something in mind that cause a shift in 2004 in the housing bubble.

That wasn't me. I believe it was bk3k.

fortune cookie say: better a delay than a disaster

fortune cookie say: better a delay than a disaster

R.W.E. of the J.B.O. wrote:As for your tax statement, if you're feeling like being reasonable, you can't ignore the fact that the population was increasing during the years revenue was decreasing. So what do you look at? You look at what changed. The population growth didn't change, so what did?

Hmm. Could it have been...tax cuts? Just sayin...

Tax cuts get lazy pols re-elected. With any luck, they'll ride their golden parachutes out of office before the 800-pound vulture comes home to roost.

Here's another theory...

In the years in question, the housing bubble was rocketing ahead, as was the home equity loan campaign, hugely buoyed by not only rampant overvaluation of homes, but significant relaxing of the standards as to how much equity was lendable against. So-called "Money" was flying around as if it was raining from heaven.

Suddenly, enormous sectors of taxable income were shielded from taxation as the money went into tax-exempt mortgages and HE loans.

Would this have significantly reduced revenue? Hell yes. Why did our leaders allow it? Greenspanish bull-market optimism. Dear God, we all bought into it. What fools we were.

In the end, it's all a major lesson in capitalism gone horribly awry. No, it doesn't mean I have sided with the bleedingheart treehuggers. But I now have a much more levelheaded notion now about what unfettered capitalism is capable of. It can be terribly abused if we allow those who can to do so, and we did...and they did. We are now essentially a feudal state as a result.

With all due respect to most of you here...many of you were hardly even out of college when all this was picking up steam a decade ago. You can now sit back, quote figures, and convince yourself it's all so simple, all so easy to analyze now, and just pick "your side". You didn't know America from an experienced adult's perspective before all this recent silliness commenced.

As teens, and even as 20-somethings, most of you were mostly clueless about what was really going on out there, and the rest were mildly aware at best, with zero real experience to compare against or draw from. Your educations did not make you instant experts. Frankly, in many ways, the isolation and lockstep conformity of institutional education made you even less aware of the big picture.

Edited 1 time(s). Last edited Tuesday, August 10, 2010 10:39 PM

I think the glut of mortgages and HE loans was one factor, yes. I'd be hesitant to say the only factor.

Credit also became much easier to obtain, both from HE loans, as well as general CC policies. I know our business saw a huge rise in CC sales during this era, as well as large purchases floated by HE loans based on equity that didn't really exist (the bubble).

I think the easy credit may been a factor in the rise in revenues in 2004...and again, a quickly rising population didn't hurt. Easy credit feeds industry, resulting in more jobs, more wages, and...more taxable income.

Meanwhile, the profits from outsourcing were also feeding the tax coffers. Slashing costs = much more taxable profit. But again...when the effects of this come home to roost, it's a dire outlook for the future.

The problem with all of this is simple, really...it was unsustainable. Once everyone was lended out, once outsourcing finished taking away the bulk of the jobs it could, and the Wall Street and real estate value collapses came, the party was very over. This is where the lofty Greenspan experiment stumbled, and badly.

Who's at fault? No one, and everyone. Both political parties fueled the fire. The biggest problem is this: it widened the gaps between the haves and have-nots (no, not welfare families, hard-working backbone of the middle class families) in a fashion we've not seen since...well, perhaps ever. This gap is now huge, and with the current world economic climate, I don't see it ever getting back to pre-2005 levels. That's a very bad thing.

If I seem ticked at those who DID profit the most from all this, I am. I am hugely disappointed and angry that a select few took obscene profits while the rest of the nation was forced to walk the plank. Look at us now...buried in debt, with horrible prospects for the future. I hope those who caused it, and those who profited from it, can sleep nights. God knows the ones they victimized can't.

Interesting article (although I don't like how it paints the defaulting borrowers in a positive light):

http://www.nytimes.com/2010/08/12/business/12debt.html?_r=2

Did the legislation "requiring" lendors to provide sub-prime mortgages extend to second mortgages/home-equity loans? If not, I'd say that the fact they were financing those hints that they would have provided the sub-primes also, even without a government "mandate"...

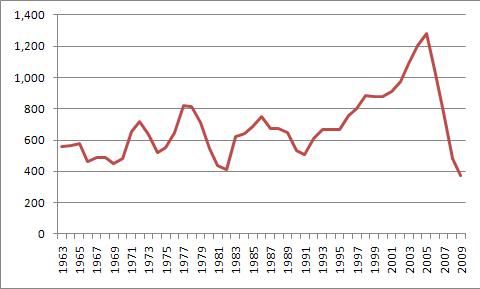

There's also a chart in there that shows mortgage increases beginning in '03, anyone know where we could find data from further back (I've looked, but can't find

)?

fortune cookie say: better a delay than a disaster

OHV notec wrote:Interesting article (although I don't like how it paints the defaulting borrowers in a positive light):

http://www.nytimes.com/2010/08/12/business/12debt.html?_r=2

Did the legislation "requiring" lendors to provide sub-prime mortgages extend to second mortgages/home-equity loans? If not, I'd say that the fact they were financing those hints that they would have provided the sub-primes also, even without a government "mandate"...

There's also a chart in there that shows mortgage increases beginning in '03, anyone know where we could find data from further back (I've looked, but can't find)?

Yes, something dire happened during this era. Banks, for some reason I do not fully understand, seemingly started lending into much more speculative situations. It's as if it was a matter of keeping up with the Joneses...once one bank(s) started to do it, they all followed suit. The question is...why? Banks used to be the most pernicious of lenders, with the highest standards. They were the hardest to borrow from.

The single most disturbing part about it, was, of course, the "false" equity that real estate overvaluation caused. Suddenly, as house "values" skyrocketed, so did the "lendable equity" in a given home. And the banks just went along with it, and handed out HE / 2nd mortgage money like candy. Why, isn't a home the most rock-solid asset possible? Well, they USED to be.

It pains me that in my adult childrens' lifetimes (they are 18 and 22), the acquisition of home equity over time will no longer be considered the best way to gain assets. Never mind that this method had been rock-solid for generations. They've been ripped off, before they even got started...the housing collapse took from them this previously rock-solid investment opportunity.

The ratio of homeowners per capita in this nation is declining for the first time ever. That's a tragedy. As more people now no longer consider a home to be the best investment they may ever make, and may even considier home ownership a dangerous potential liability should the poop hit the fan again, this trend is not expected to reverse itself soon. So another piece of the American dream falls into the abyss.

I appreciate your optimism, but no...they won't end up back where they would have been if it weren't for the bubble. My current Illinois home has reverted back to its 2001 appraised value. It is far behind what it SHOULD be valued at now had the market not gone stupid apesh!t. This is due precisely to the bubble and the mortgage fiasco putting so many cheap homes on the market currently.

At this point, I have lost 10 years of reasonable equity appreciation. When cost of living and inflation are factored in, the loss is even worse.

It will be years before the current glut of cheap real estate is absorbed to the point of expecting real estate values to again appreciate. That's your vaunted supply and demand keeping the value of my #1 investment in the basement for now, and for the foreseeable future.

So, by the time things could even be expected to again take an upward trajectory, I will be approximately 15 years behind where I WOULD have been in appreciation on this investment. To expect that 15 years of lost equity appreciation to right itself is pure folly. That money is gone, and forever. All because a select group of real estate and lending "professionals" created an entirely unsustainable Ponzi that made them rich...and almost ALL of the rest of us poorer.

Solid financial advice says "sell it now, take the loss...it's better than pumping tens of thousands of more dollars into interest payments over the next few years while the home's value stays static."

This is capitalism at its most sinister. This is how I lost faith.

Bill, just consider yourself lucky that Illinois didn't build as fast as AZ. My house is now valued

barely above it's original sale price in the late 80's. Considering that the surrounding area has since been developed from the old corn fields, that's a nearly impossible hit

I agree that prices will start back up at a normal rate, but like you, I don't see how they could possibly make up for the last 10 years lost...

fortune cookie say: better a delay than a disaster

Actually, no...I purchased it in 1995. Of COURSE it's worth more than I paid for it, lol...15 years later, with 15 years of intense interest paid to lenders, it sure as hell

BETTER be! But no matter how we spin this, the fact is, it has reverted to a value it held TEN YEARS AGO. I have lost ten years of reasonable equity appreciation that will not 'catch up' ever again. I will lose years more while the destroyed market "works itself out".

Your contention was that this will all right itself, and that my lost equity appreciation value will someday reappear:

RWE of JBO wrote: It will be a few years, but the values will end up back where they would have been if it weren't for the bubble.

You are incorrect...it will not.

Capitalism sure as hell DID cause this loss of wealth among the rank and file, while lining the pockets of those positioned to profit from all our losses...ruthless bankers and real estate people (agents and speculative owners) did it in the zeal for previously unprecedented profit. No matter what government regulatory changes helped fuel this fire, these individuals acted unconscionably, for their own pure gain. They got RICH. Most of them knew MUCH better. They did NOT act out of a concern for the common good. This is how Greed raises its ugly head, and can create thieves and liars out of otherwise honorable individuals. Greed is the one aspect that pure, unabated Capitalism has no effective answer for. We've all just witnessed this in outrageous action.

I was an unabashed supporter of pure Capitalism for decades prior to this. Now, I am much more enlightened, and much more wary. No, its not just a raw ass over my own losses...it's what I've witnessed nationwide that perturbs me. I've not lost faith completely by any means...I've just lost that starry-eyed abject loyalty to capitalism-at-all-costs I used to have.

Capitalism took a real black eye here lately, and I'm far from alone in this belief. We're all much more aware now.

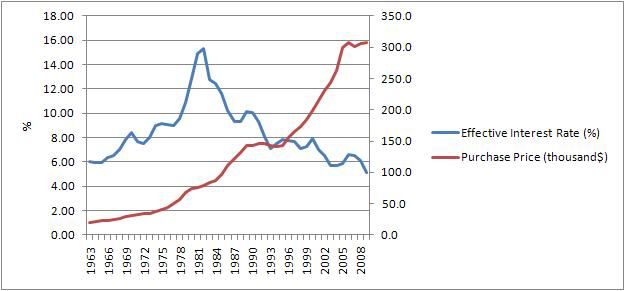

Bill, although 2003 looks to be the start of the highest rate of increase, 2000+ looks to be steep enough to say that certainly wasn't enough to provide the '03 tax revenue increase Quik was talking about.

fortune cookie say: better a delay than a disaster

R.W.E. of the J.B.O. wrote:Take Back the Republican Party wrote:Your contention was that this will all right itself, and that my lost equity appreciation value will someday reappear:

RWE of JBO wrote: It will be a few years, but the values will end up back where they would have been if it weren't for the bubble.

You are incorrect...it will not.

You're misunderstanding here. I am not saying you will get back the last 10 years of value, but that what you gained was inflated to begin with, so you are losing an inflated value that your house never really had.

No, I don't misunderstand...but I fear you do. I don't care about the "bubble" value. That was unrealistic as hell, and I am not a fool. The 2001 value I am benchmarking here was well before any bubble.

Had the "bubble" not occurred, my house would have been instead appreciating slowly, but steadily, for the last ten years. That was the promise of American home ownership for the last few generations, that it was the most rock-solid investment you can make, and that it would always appreciate in value. Well, I've lost ten years of that

reasonable appreciation (please note that I've continually said REASONABLE to differentiate from the "bubble" insanity) to this bubble and fiasco, and I'll lose a few more before its over. My investment has not even kept pace with INFLATION.

So, yes, your statement was incorrect...house values will NOT

"end up back where they would have been if it weren't for the bubble". The only thing that could replace this 10 to 15 years of lost REASONABLE appreciation would be

...another bubble!

R.W.E. of the J.B.O. wrote:

In the end, it was the government meddling that made it all possible, and more government meddling is not going to fix it, it is only going to keep it down.

I could almost side with you on this if it weren't for the fact that you couple the term "government meddling" with your politics EXCLUSIVELY. Oh, if only life were that simple, that one side does everything right, and one does it all wrong. No matter what democrats do, you condemn it as "meddling" or any of many other disparaging terms you toss at them. Meanwhile, anything a republican administration has done is golden.

Aren't you smarter than that?

Actually, in that chart Notec posted, I don't see a bubble "starting in the early-mid 90's." Not unless you consider the reasonable yearly appreciation from 1963 to 1988 shown to also be a "bubble", which it most certainly was not. Note that both slopes are similar (up until 2002 anyway), and the only discerning feature is that the average price of a home sold in the years 1988-1994 rather held steady (flatlined). If one takes away this flatline section, and studies just the slope, one can see that the rate of "value gain" started to be practically vertical in 2002 and up.

This was the bubble, and

THIS is when obscene profit-taking begain.

In any case, a select few made big bank, and the rest of us got fcuked. I've done little but pay bankers' salaries with my mortgage for the last ten years, as I saw ZERO equity gain during this time from appreciation, and I simultaneously lost real equity via inflation. I'm glad they were able to pay

their bills with

my money. There went about a hundred-fifty grand in mortgage payments, some of which I'd sure like to have seen come back in equity appreciation, like my parents and their parents and their parents did.

Greenspan is an idiot for failed polices that put an entire generation's assets at risk. Financial markets are a legalized Ponzi at times like that. That's my least favorite side of capitalism.